Carbon Accounting 101

There it is, in your calendar in that shade of red that shouts ‘important’, a meeting scheduled to allocate tasks for Greenhouse Gas (GHG/C02) reporting! Grab a cup of coffee before the meeting; you’ll need to be well caffeinated going in. If this has already happened in your organization then you’ll know how much data mining this requires, and I’d love to hear about your experience (see begging note at the end).

Why do we need to report GHG (C02) emissions?

There are regulatory (Federal, State & International) reporting requirements, customer requirements, leadership requirements, voluntary reporting as a business efficiency metric and risk management issues (SEC 10K disclosure requirements) to name an important few. Whatever the drivers for reporting carbon emissions, a lot of the work usually falls to the facilities/real estate folks.

If you have not been asked yet, this is a great opportunity to get out in front of this. If you’re currently grappling with this issue I hope you gain something of benefit from this and future blogs.

As of January, 2010 over 3,000 global companies report to the CDP (Carbon Disclosure Project), the Dow Jones Sustainability Index (DJSI) which rates companies by industry and sustainability performance and the FTSE4Good (Financial Times Stock Exchange index – UK) that rates companies for corporate responsibility and is used by ethical investors all over the world.

What do we need to report?

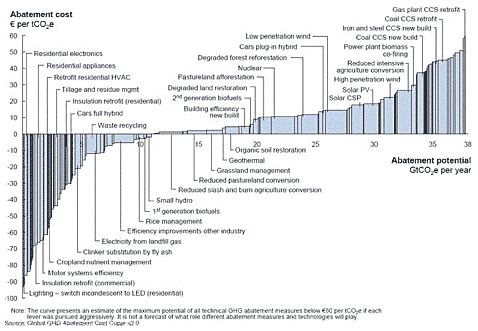

Under the GHG Protocol GHG emissions are expressed as tCO\2e.

t = metric tonnes (the metric system is used by the rest of the world, get over it)

CO2e = CO2 equivalent. This is the GWP (Global Warming Potential) as calculated and expressed as CO2 equivalency (e.g. 1 tonne of methane is equivalent to 21 tonnes of C02 (21 times more global warming potential) for an apple to apple comparison of various compounds.

There are six main GHG’s reported:

- Carbon dioxide (CO2).

- Methane (CH4).

- Nitrous Oxide (N2O).

- Hydrofluorocarbon (HFC)

- Perfluorocarbons (PFC)

- Sulfur Hexafluoride (SF6)

Baseline Year:

All emission reporting starts from a baseline year. This may be given to you, if you have any input into the base year, pick a year where you have good data. You’ll never have all the data you need easily available. Ask yourself; how much refrigerant did you use in 2006 broken down by chemical type (e.g. Scope 1: R-134A is a Hydrofluorocarbon with a GWP of 5,000)? How much diesel fuel was used in 2004 for testing of your emergency generators (also Scope 1)? You see what I’m getting at?

If you’re lucky your utility will have automated your facility energy use; expressed in Kwh in Excel or a similar format going back 5 or more years. If you have facilities in other parts of the country and internationally, you may face additional challenges in getting the information. After doing this for nearly 5 years, getting accurate data is by far the biggest issue we see. FM departments need to start accumulating this data and archiving it in a format that is easily accessed and as up-dated as necessary. GHG reporting is usually done Q1/Q2 every year, and don’t think it’s going away any time soon. We’re seeing a push for much more granularity in the data collected. Is this a chance for you to shine even brighter?

Scope Boundaries:

When reporting voluntarily the organization gets to set the reporting boundaries (However; the standards are expected to increase year on year).

- Scope 1: Direct emissions at owned facilities usually from on-site generation or process (burning fossil fuel and/or emissions of chemicals). These are directly under the control of the organization, as you select the fuel source or chemicals used and you own the process (e.g. fleet vehicles that are owned are scope 1).

- Scope 2: These are usually indirect emissions, and electricity is the most common scope 2 reported. The utility selects the fuel source and as such the emission has to be calculated based on the fuel mix used in that region by that utility. However if you also manage travel as part of your scope of services; business travel is also scope 2 based on miles traveled and mode of transport (mostly jet and vehicle fuel).

- Scope 3: This is everything else. If you take a close look at the FM supply chain there are a great many items that impact your emissions. Scope 3 is the next step as we work towards reducing total emissions. Extra credit: Asking your suppliers for their GHG reports as part of the *procurement process sends a strong signal that you’re serious (sends the right message to your boss too).

- *Wal-Mart did this recently and it sent a strong message to their suppliers and greatly changed the way they used resources. The data so far indicates that there has been no increase in supplier costs or availability of products.

What next?

That’s where you come in. I need you to tell me what you want to hear about; is it carbon accounting 102, abatement strategies or other sustainability issues? I’ll be happy to group the questions into a sort of FAQ section of this blog, but in order to do that I need your FAQ’s. To prime the pump, I’ll incentivize you by offering a Starbucks gift card ($10) for the *best FM sustainability question. You’ll need the extra caffeine once you start down the GHG road.

*I will be the sole arbiter of the best question and my decision is final (unless my wife disagrees, then we’ll go with that).

Extra reading credits:

Carbon Disclosure Project: https://www.cdproject.net/en-US/Pages/HomePage.aspx

Walmart / CDP: http://walmartstores.com/Sustainability/7759.aspx

Greenhouse Gas Initiative Protocol: http://www.ghgprotocol.org/

World Resources Institute GHG: http://www.wri.org/project/ghg-protocol

World Business Council on Sustainable Development: http://www.wbcsd.org/templates/TemplateWBCSD5/layout.asp?type=p&MenuId=MTAxMQ&doOpen=1&ClickMenu=LeftMenu

Bruce Thorpe.

Bruce is a Senior Associate at WSP Sustainability & Energy http://www.wspenvironmental.com/ . He leads WSP’s Sustainable Real Estate and Workplace practice in North America and is based in San Francisco.